Competitive look-alike

Demi-fine / vermeil / sterling silver. Many DTC collections converge on near-identical minimal staples (basic bands, similar chains). Oomiay's edge: sculptural forms, 2.5 micron plating, warranty-backed quality.

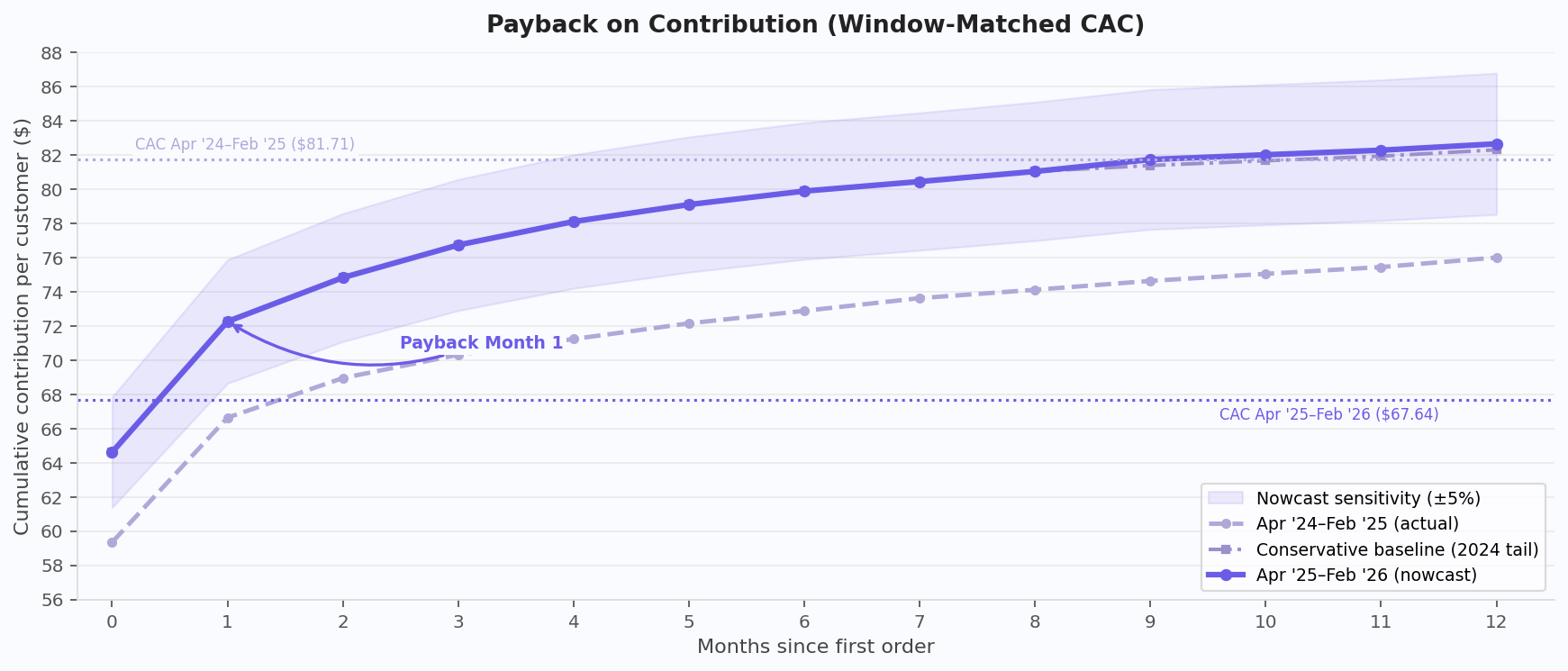

Payback on contribution

- Apr '25 – Feb '26 cohorts: contribution payback vs current CAC ($67.64) — Month 1.

- By Month 9, 2025 cohort contribution LTV ($81.72) surpasses the prior-year CAC benchmark.

Apr '25–Feb '26 windows are post-pivot. LTV: incremental maturity-weighted nowcast from Polar cohorts, 74.0% net contribution margin (Finaloop). Apr '24–Feb '25 baseline. Tail (Mo 10–12): 2024 observed increments × 0.7 shrinkage. Payback = first month cumulative contribution ≥ window-matched CAC.

CAC + new customer AOV (monthly, window-matched)

- Blended CAC (Apr–Feb): $67.64 vs $81.71 −17.2%

- New customer AOV (Apr–Feb): $91.32 vs $81.93 +11.5%

- Monthly table shows the improvement is broad-based, not a single-month artifact.

Window: Apr '25–Feb '26 vs Apr '24–Feb '25 (window-matched). Blended CAC = total paid spend ÷ new customers ('24: $1.92M / 23,498; '25: $1.45M / 21,425). New customer AOV = new customer sales ÷ new customers (first order; from Customer Metrics export). Weighted average column is the window summary used in the core deck.

Financial history + accounting basis

- 2024+ is accrual via Finaloop (consistent basis starting Jan 1, 2024).

- Starting mid-March '25: deliberate reset — tightened catalog, cleared legacy inventory, rolled out quality upgrades across the core assortment.

- TTM (Mar '25–Feb '26): near-breakeven (−$40K EBIT, −1.4% margin) and +$155K EBIT ex-founder comp (+5.3% margin).

- TTM EBIT improved +$315K vs prior TTM (Mar '24–Feb '25 = −$355K, −11.8% margin).

2022–2023 are cash basis; 2024+ is accrual via Finaloop. EBIT ex-founder comp adds back $195K annual total founder comp — three full-time operator-founders at $65K each. TTM = Mar '25–Feb '26. Mar '25 includes intentional catalog reset and inventory clearance.

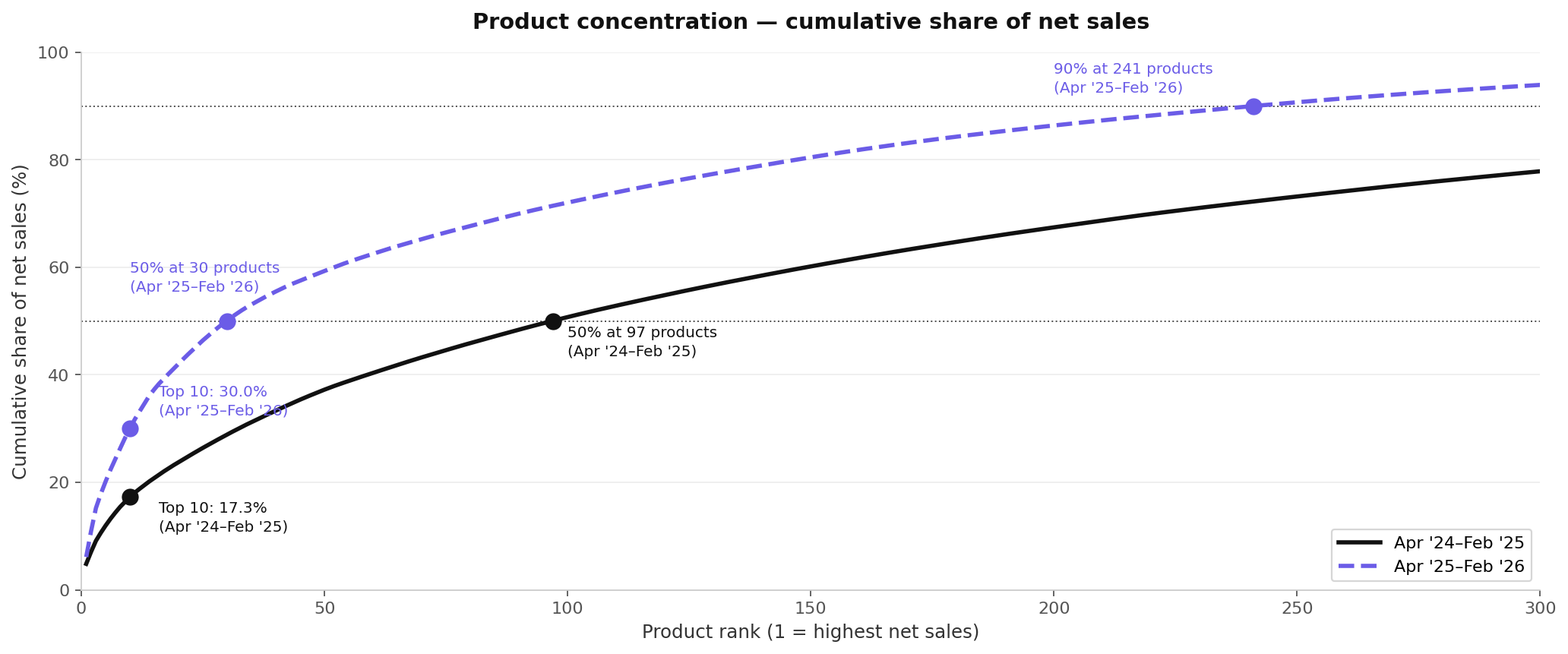

SKU focus + inventory discipline

- Concentration increased post-reset: Top 10 = 30% of net sales (vs 17% in prior year).

- Fewer "winners" drive the business: 50% of net sales from 30 products (vs 97 in prior year).

- Enables deeper buys on proven styles (fewer long-tail bets) → lower aged inventory risk + more predictable working capital.

Net sales by product, Apr '25–Feb '26 vs Apr '24–Feb '25. Products ranked by net sales; chart shows cumulative share of net sales by product rank. Post-reset refers to the mid-March '25 catalog reset; Apr–Feb window reflects the clean post-reset period.